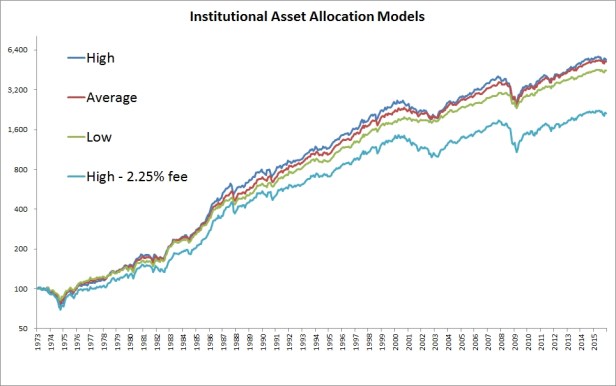

The difference between the most and least aggressive portfolios is a whopping 0.53% a year…Overlay a simple 1% management fee on the most aggressive portfolio and look again at the returns…you have turned the highest returning allocation into the lowest returning allocation. -Meb Faber

The performance of various asset allocations from a low equity allocation of 44% to a high equity allocation of 74% tend to converge over a long time horizon. Any benefit from a smarter (i.e. luckier) asset allocation are blown away by fees. In fact, subtracting a 1% advisory fee (advisory fees, kickbacks, churning, other hidden costs) from even the best performer resulted in a huge drag on performance:

If your advisor uses average-priced mutual funds or separately managed accounts, the drag on performance over time is even more dramatic:

So how much longer will you be working to make up for your advisory fees and mutual fund fees? You could be working more than a decade longer.

- If you invest $500k in low-cost funds that return 7% over 25 years, you will accumulate a balance of $2.7M.

- If you invest $500k with an advisor that takes 1% annually over 25 years (through advisory fees, kickbacks, churning, other hidden costs), you will wind up with a balance of $2.1M. You have to work 4 years longer to reach the same balance.

- If you invest $500K with an advisor that skims 1% over 25 years (through advisory fees, kickbacks, churning, other hidden costs) and uses mutual funds or money managers that take another 1.25% off the top, you will wind up with a balance of only $1.6M. You have to work 12 years longer just to keep up with your peers!

How using a traditional financial advisor will cost you over a million dollars in graphic detail: How Advisory Fees Cost $1 Million over 30 Years.

Click here to learn how to transfer your investment accounts to get out from under the oppressive fees.

-AK

To follow this blog, please enter your email address at the end of this post (on mobile) or upper right corner (on desktop). Thanks for reading!