magical thinking: Irrational belief that one can bring about a circumstance or event by thinking about it or wishing for it; normal in preschool children, it also occurs in schizophrenia.

-Medical Dictionary for the Health Professions and Nursing

When you purchase an annuity, you don’t get an itemized bill for the commission or the billions in overhead costs to run the insurance company that sells the annuity.

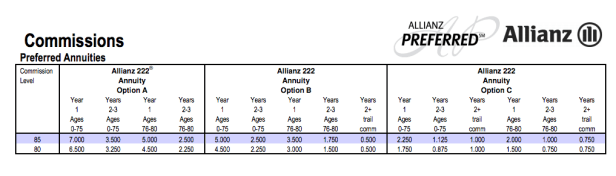

In the figure below, the numbers represent percentages of the total amount of money you put into the annuity that is paid to your salesperson in commission. Who pays that 7% commission in Year 1? Who pays that 3.5% commission in Year 2? Who pays that 3.5% in Year 3? You guessed it, it’s you!

No, you won’t see commissions deducted directly from your annuity balance. Your money goes into one big pool of money with everyone else’s money. Your account statements will show an imaginary “credit” that is attributable to you. It’s not set aside in some magical pot of money at the end of the rainbow, guarded by leprechauns. After all, there are so many people who rely on your annuity premiums to make their McMansion mortgage payments that it’s really for the best that you continue to believe the whole magical pot of money fairy tale, leprechaun’s included.

Your return = (initial deposit) + (market earnings) – (commissions) – (operating expenses and corporate debt obligations) – (corporate profits, bonuses, and shareholder dividends) – (catastrophic trading losses on shitty leveraged investments) – (corporate taxes) – (fines/fees for improper behavior)

Despite all these fees and expenses, annuities are NOT guaranteed, regardless of the AAA-rating of the company selling them. AIG stands out as the best example for why annuities are NOT the best way to protect again extreme financial outcomes. AIG was the AAA-rated company that, almost overnight, found itself in need of a $182 billion bailout from the Federal government in 2009. If the Federal government had not bailed out AIG, the annuity owners would have been out of luck, receiving a fraction of what they were promised.

Based on current returns offered by annuity plans, you can get the same return with much less risk of insurance company insolvency by investing 80% in an array of U.S. Treasury bonds (in tax-deferred accounts) and AAA-rated municipal bonds (in taxable accounts) matched to your longevity and 20% in global equities. When you buy a bond, you own it, and it is backed by the government. When you buy an annuity, what do you really own?

— AK